(a) Who can be the primary Authorized Signatory?

A primary Authorized Signatory is the person who is primarily responsible to perform action at the GST Common Portal on behalf of the taxpayer. All communication from the GST Common Portal relating to taxpayer will be sent to the primary Authorized Signatory.

Type of Business |

Who can be the Authorized Signatory? |

Proprietor |

The proprietor or any person authorized by the proprietor |

Partnership |

Any authorized partner or any person authorized by the partners |

Company, LLP,

Society or Trust |

The person authorized by Board or Governing Body can act as Primary Authorized Signatory |

In case there is a single Authorized Signatory for a business entity, the single Authorized Signatory will be assumed to be the primary Authorized Signatory.

In case there are multiple Authorized Signatories for a single business entity, one Authorized Signatory need to be designated as primary Authorized Signatory. The e-mail address and mobile number of the Authorized Signatory needs to be provided during enrolment. The Authorized Signatory or Primary Authorized cannot be Minor in age.

(b) The data auto-populated from GST database, during enrolment process, which has been migrated and authenticated from PAN database are given following:

• PAN of the Business

• Legal Name of Business

• Name of the State

• Reason of liability to obtain registration

(c) In the Enrolment Application, jurisdictional mapping is also given. Taxpayer may select their jurisdiction. However, officers have been given power to modify it in case wrong jurisdiction has been selected by the taxpayer.

(d) Principal Place of Business and Additional Place of Business:

Principal Place of Business is the primary location within the State where a taxpayer’s business is performed. The principal place of business is generally the address where the business’s books of account and records are kept and is often where the head of the firm or at least top management is located.

Additional Place of business is the place of business where taxpayer carries out business related activities within the State, in addition to the Principal Place of Business.

(e) HSN and SAC code:

HSN stands for Harmonized System of Nomenclature which is internationally accepted product coding system used to maintain uniformity in classification of goods.

SAC stands for Service Accounting Codes which are adopted by the Central Board of Excise and Customs (CBEC) for identification of the services.

(f) DSC v/s e-sign:

It is compulsory that all application of registration will be digitally signed. However, class II or III Digital Signature Certificate is mandatory for Companies, Foreign Companies, Limited Liabffity Partnership (LLPs) and Foreign Limited Liability Partnership (FLLPs). Other taxpayers, may use either e-signing or DSC.

(g) Submission of complete application:

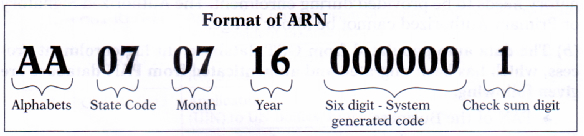

Once complete application is submitted, an Application Reference Number (ARN) is generated by the System. It is a unique number assigned to each transaction completed at the GST Common Portal. It will also be generated on submission of the Enrolment Application that is electronically signed using DSC. ARN can be used for future correspondence with GSTN. |

@ Rs.700")

@ Rs.700")

@ Rs.600")

@ Rs.550")