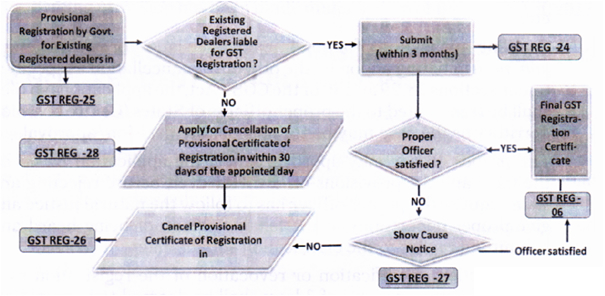

Sec. 139 of CGST Act and the equivalent sections of SGST and UTGST provides that on the appointed day (the day GST is rolled out):

i. Every person registered under any of the existing laws which have been subsumed under GST and having a valid Permanent Account Number, shall be issued a certificate of registration on provisional basis.

ii. the Enrolment application of the taxpayers will be verified by the jurisdictional officers and if found deficient or not fulfilling the conditions which are prescribed for compliance, the same may be cancelled.

In case enrolment application is submitted in complete form or subsequently it is completed by the taxpayer and submitted with DSC or e-sign, the proper officer may verify and issue final registration with GSTIN as permanent registration certificate.

Flow diagram of enrolment process: |

@ Rs.700")

@ Rs.700")

@ Rs.600")

@ Rs.550")