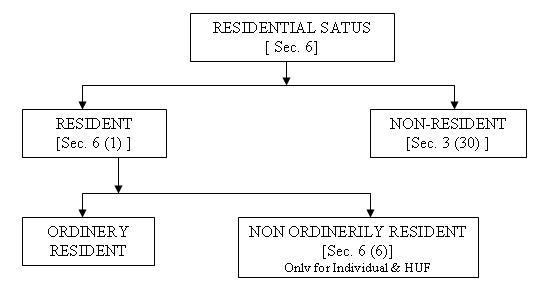

RESIDENTIAL STATUS OF AN ‘INDIVIDUAL’

An individual may be …

(a) Resident and ordinarily Resident in India

(b) Resident and not-ordinarily Resident in India;

(c) non-resident in India.

(a). Resident and Ordinary Resident [ Section 6 (1), 6(6)(a) ]

To determine the Residential Status of an Individual, [Section 6 (1)] prescribes Two Test. An individual who fulfils any one of the following Two Tests is called Resident under the provisions of this Act. These Tests are :

Test No. 1. Stay in India for 182 days or more.

If an individual has to become Resend of India during any previous year, his / her personal stay in India during that year is a must although the number of days of stay differs in the two tests. It means that if an individual does not stay in India at all in any previous year , he cannot be Resident of India in that year. Stay in India means that the individual should have stayed in India territory and anywhere ( cities, villages, hills, even Indian territory waters ) for such number of days.

The period of 182 days need not be at a stretch. But physical presence for an aggregate of 182 days in the relevant previous is enough. The Status of Resident is not linked with any particular place or town or house.

The onus to prove the number of days of stay in India lies on the assessee. It is for him to prove, if he desires to be taxed as non-resident or not ordinarily resident.

Test No. 2. Presence for 365 days during the Four preceding Previous Year and 60 days or more in that relevant Previous Year.

A person may be frequent visitor to India. In his case, the residential status will be determined on the basis of his presence in India for 365 days in four years immediately preceding the relevant Previous year. Along with this his presence for 60 days during the relevant previous year is another essential conditions to be fulfilled. The purpose, object or reason of visit to and stay in India has nothing to do with the determination of residential status.

Explanations :

For Indian Citizen going abroad on a Job or as a member of crew of an Indian ship [Explanation (a) ]

In case of Indian citizen who is going outside Indian for a Job and his contact for such employment outside India has been approved by the Central Government or he is a member of crew of an Indian Ship, Test (a) U/s 6(1) remains same but in Test (b) words ‘60 days’ have been replaced to 182 days.

For Indian Citizens and Persons of Indian Origin [Explanation (b) ]

For such person Test (a) remains the same but in Test (b) ) words ‘60 days’ have been replaced to 182 days.

( A person shall be deemed to be of Indian origin if he or either of his parents or any of his grand parents was born in India or undivided India .) |

@ Rs.700")

@ Rs.700")

@ Rs.600")

@ Rs.550")