Taxable Incomes under the head 'Income from Other Sources' [Section 56(2)] |

Sub-section (2) of section 56 specifies 9 (nine) incomes which are always taxable under the head “Income from other sources”. |

-

Taxability of Dividend Income [Section 56(2)(i)]

-

Winnings from Lotteries, Crossword Puzzles, Horse Races and Card Games [Section 56(2)(ib)]

-

Interest on Securities under the head 'Income from Other Sources' [Section 56(2)(id)]

-

Income from Letting Out of Machinery , Plant or Furniture [Section 56(2)(ii)]

-

Income from Composite Letting of Machinery, Plant or Furniture and Buildings [Section 56(2)(iii)]:

-

Share Premium in excess of the Fair Market Value to be treated as Income [Section 56(2)(viib)]

-

Interest on Compensation or Enhanced Compensation [Section 56(2)(viii)]

-

Forfeiture of Advance Received for Transfer of a Capital Asset to be Taxed under the head "Income from Other Sources" [Section 56(2)(ix)]

-

Income of any person to include not only gift of money from any person(s) but also the gift of property (whether movable or immovable) or property acquired for inadequate consideration [Section 56(2)(x), w.e.f. A.Y. 2018-19]

|

1. Taxability of Dividend Income [Section 56(2)(i)] |

1. What is Dividend Income

Dividend in its ordinary connotation means the amount paid to or received by a shareholder in proportion to his shareholding in a company out of the total sum so distributed.

Dividends can be of three types:

- Dividends declared by a domestic company.

- Dividends or any other income distributed by Unit Trust of India.

- Dividends declared by a foreign company.

w.e.f. assessment year 2017-18, any income by way of dividends chargeable to tax in accordance with the provisions of section 115BBDA shall not be exempt under section 10(34) even if the tax has been paid on that dividends by the domestic companies under section 115-O.

Dividend which is exempt under section 10(34) includes deemed dividend but shall not include deemed dividend mentioned in section 2(22)(e), i.e., loan/advance given by a closely held company to a specified shareholder/concern.

Since dividends other than chargeable to tax under section 115BBDA received from a domestic company shall be exempt, no deduction of any expense shall be allowed from such dividends.

Dividend from a foreign company or deemed dividend, mentioned under section 2(22)(e) shall, however, be taxable under the head "Income from Other Sources".

Since dividend is exempt in the hands of the recipient, the domestic company shall be liable to pay additional income-tax on the amount declared, distributed or paid by such company by way of dividends, whether interim or otherwise, whether out of current or accumulated profits.

Exemption of income from Units [Section 10(35)]:

Like in case of dividend, section 10(35) provides that any income received in respect of—

- units from the Administrator of the specified undertaking, or

- the specified company, or

- a Mutual Fund specified under clause (23D)

shall be exempt.

2. Accumulated Profits for Distribution of Dividend

Under section 2(22), the following payments or distribution by a company to its shareholders are deemed as dividend to the extent of accumulated profits of the company (it may be noted that these payments may not be “dividend” under the Companies Act):

-

any distribution entailing the release of company’s assets ;

-

any distribution of debentures, debenture-stock, deposit certificates and bonus to preference shareholders ;

-

distribution on liquidation of company ;

-

distribution on reduction of capital ; and

-

any payment by way of loan or advance by a closely-held company to a shareholder, holding substantial interest, provided the loan should not have been made in the ordinary course of business and money-lending should not be substantial part of the company’s business

It is, therefore, essential to discuss meaning and scope of the expression “accumulated profits”.

(A) Does 'Accumulated Profits' include Current Profit -

-

Accumulated profit means profit available to the company, on the date of distribution, after deducting all expenses including income-tax expenses.

-

In case of a company, which is not in liquidation, it includes all profits of the company up to the date of distribution or payment.

-

In the case of a company in liquidation, it includes all profits of the company up to the date of liquidation. Where, however, the liquidation is consequent on the compulsory acquisition of a company’s undertaking by the Government or a Government company, accumulated profits do not include any profits of the company prior to the three successive years immediately preceding the previous year in which such acquisition took place. For instance, if accounting year of a company is financial year and compulsory acquisition takes place on March 13, 2018, accumulated profits will exclude profits accumulated up to March 31, 2014.

(B) What is basis of computing Accumulated Profit -

Accumulated profits are computed on the basis of commercial profits and not on the basis of assessed income.

(C) Depreciation Deduction for Computing Accumulated Profit-

While calculating “accumulated profits” an allowance for depreciation at the rates provided by the Income-tax Act itself has to be made by way of deduction.

(D) Balancing Charge for Computing Accumulated Profit -

Balancing charge assessable under section 41(2) does not form part of accumulated profits as it is not commercial profit but it is withdrawal of depreciation when the asset is sold for a price higher than the written down value.

(E) Tax-Free Income for Computing Accumulated Profit-

Accumulated profits include tax-free income, e.g., agricultural income. However, receipts of capital nature are included in accumulated profits only if such receipts are chargeable to tax under the head “Capital gains” in the hands of recipient company.

(F) General Reserves for Computing Accumulated Profit-

Accumulated profits include general reserve.

(G) Provisions for Computing Accumulated Profit-

Provisions for taxation and dividends do not form part of accumulated reserve.

(H) Addition made by Assessing Officer for Computing Accumulated Profit-

Addition made by the Assessing Officer on account of concealed income forms part of accumulated profit.

(I) Accumulated Profits of Amalgamating Company -

In the case of an amalgamated company, accumulated profits or loss in the hands of the amalgamated company shall be increased by the accumulated profits of the amalgamating company (whether capitalised or not) on the date of amalgamation.

3. Disbursements by the Company to the Shareholders, to the extent of Accumulated Profits.

(A) Distribution of Accumulated Profits Entailing Release of Company's Assets [Section 2(22)(a)]

Under sub-clause (a) of section 2(22), any distribution by a company of its accumulated profits (whether capitalised or not) is dividend, if it entails the release of company’s assets.

In other words, there are two conditions prescribed by this clause —

-

first distribution should be from accumulated profits (not from capital) and

-

secondly, such distribution must result in the release of the assets by the company.

When a company distributes bonus shares to equity shareholders by capitalising its profits, then there is no release of assets and consequently, bonus shares are not treated as dividend.

(B). Distribution of Accumulated Profits in the form of Debentures, Debenture Stock [Section 2(22)(b)]

Under this clause, the following two distributions are treated as dividend to the extent of accumulated profits (whether capitalised or not) of the company:

-

distribution by a company to its shareholders (whether equity shareholder or preference shareholder) of debentures, debenture stock, or deposit certificates in any form, whether with or without interest; and

-

distribution by a company to its preference shareholders of bonus share.

It is worthwhile to note that under the aforesaid circumstances, distribution amounts to dividend even if there is no release of assets at the time of distribution.

(C). Distribution of Accumulated Profits at the time of Liquidation [Section 2(22)(c)]

Under sub-clause (c), any distribution made by a company to its shareholders on its liquidation is treated as dividend to the extent to which such distribution is attributable to the accumulated profits (whether capitalised or not) of the company immediately before its liquidation.

Under sub-clause (c), the following are, however, not treated as dividend:

-

any distribution in respect of preference shares issued for full cash consideration; and

-

any distribution insofar as such distribution is attributable to the capitalised profits of the company representing bonus shares allotted to its equity shareholders during 1964-65.

(D). Distribution of Accumulated Profits on the Reduction of its Share Capital [Section 2(22)(d)]

Any distribution by a company to its shareholders on the reduction of capital is treated as dividend to the extent the company possesses accumulated profits (whether capitalised or not).

For this purpose, profits of the company, upto the date of resolution permitting the reduction of share capital, shall form part of the accumulated profits.

However, the following are not treated as dividend under this clause:

-

any distribution out of accumulated profits which arose up to the previous year 1932-33;

-

any distribution in respect of preference shares issued for full cash consideration; and

-

any distribution in so far as such distribution is attributable to the capitalised profits of the company representing bonus shares allotted to its equity shareholders during 1964-65.

(E). Distribution of Accumulated Profits by way of Advances or Loans to certain Shareholders / Concerns [Section 2(22)(e)]

Any payment by a company, (other than a company in which the public are substantially interested), of any sum (whether as representing a part of the assets of the company or otherwise) by way of advance or loan, to the extent of accumulated profits (excluding capitalised profits) to:—

-

an equity shareholder, who is beneficial owner of shares holding not less than 10% of the voting power; or

-

any concern in which such shareholder (holding not less than 10% voting power) is a member or a partner and in which he has a substantial interest i.e. holding 20% voting power or 20% shares in the concern; or

-

any person, on behalf, or for the individual benefit, of any such shareholder. Such shareholder here means a shareholder who is beneficial owner of share holding not less than 10% voting power.

This provision is applicable only to companies in which the public is not substantially interested i.e. closely held companies. Further, such loan and advance given to such person shall be deemed to be dividend only to the extent to which it is shown that the company possesses accumulated profits on the date of loan, etc. (exclusive of capitalised profits).

-

"Concern" means a HUF, a firm, an AOP or BOI or a company.

-

Whether loan or advance is given on interest or not, does not effect the applicability of section 2(22)(e).

|

4. Key Points regarding the Taxability of Dividend U/s 56(2)(i)

Here are the key points regarding the taxability of dividend income under this section:

Applicability:

This provision applies to individuals, HUFs, and firms, among others, who receive dividend income. It does not apply to companies, as dividend distribution tax (DDT) was applicable to companies distributing dividends.

Tax Rate:

As of my last update, dividend income received by individuals and HUFs is generally taxable at a flat rate of 10%. This rate is exclusive of any applicable surcharge and cess.

Threshold Limit:

As per the provisions of Section 56(2)(i), dividend income received by an individual or HUF exceeding Rs. 10 lakh in a financial year is taxable. Any dividend income below this threshold is not subject to tax.

Reporting:

Taxpayers are required to report dividend income in their income tax returns and disclose the details of the dividend income received during the financial year.

Exemptions:

Certain dividends, such as those received from Indian companies on which dividend distribution tax (DDT) has already been paid, may be exempt from tax in the hands of the recipient. However, the taxation of dividends has undergone significant changes, including the abolition of DDT for companies and the introduction of the Dividend Income Tax (DIT) in the hands of the recipients. Therefore, it's essential to refer to the latest tax rules and notifications to determine the exact tax treatment of dividend income.

Dividend Distribution Tax (DDT):

Before the changes in the taxation of dividends, companies were liable to pay DDT on the dividends they distributed to shareholders. However, with the abolition of DDT, the taxation of dividends shifted to the recipients, i.e., individuals, HUFs, and other entities.

TDS (Tax Deducted at Source):

As per Section 194 of the Income Tax Act, companies are required to deduct TDS at the rate of 10% on dividend payments exceeding Rs. 5,000 to individual shareholders. The TDS deducted can be adjusted against the final tax liability of the shareholder.

5. Deductions for Expenses from Dividend Income [Section 57(i) and 57(iii)]:

The following expenses can be claimed as deductions from gross dividend income other than the dividends referred to in section 115-O:

-

Collection charges:

any reasonable sum paid by way of commission or remuneration to a banker or any other person for the purpose of realising the dividend.

-

Interest on loan:

Interest on money borrowed for purchasing the shares can be claimed as a deduction. The interest can be claimed even if no income is earned by way of dividend on such shares. It has been held by the Supreme Court that if the expenditure has been laid out for the purpose of earning the dividend income then whether income is actually earned or not is immaterial and deduction on account of interest can be claimed.

-

Any other expenditure:

Any other expenditure, not being a expenditure of a capital nature, expended wholly and exclusively for the purpose of making or earning such income, can be claimed as a deduction.

| Since dividends referred to in section 115-O (i.e. dividends covered under section 2(22)(a), (b), (c) and (d) are exempt in the hands of the shareholders, no deduction of any expense referred to in section 57 shall be allowed. |

6. Tax on certain Dividends received from Domestic Companies [Section 115BBDA]

(1) Dividend in aggregate exceeding Rs.10,00,000 received by certain persons to be taxed at the special rate of 10% [Section 115BBDA(1)]:

Notwithstanding anything contained in this Act, where the total income of a specified assessee, resident in India, includes any income in aggregate exceeding Rs. 10,00,000, by way of dividends declared, distributed or paid by a domestic company, the income-tax payable shall be the aggregate of—

-

the amount of income-tax calculated on the income by way of such dividends in aggregate exceeding Rs.10,00,000, @ 10%; and

-

the amount of income-tax with which the assessee would have been chargeable had the total income of the assessee been reduced by the amount of income by way of dividends.

(2) No Deduction to be allowed from Dividend Taxable at Special Rate under Section 115BBDA(1) [Section 115BBDA(2)]:

No deduction in respect of any expenditure or allowance or set off of loss shall be allowed to the assessee under any provision of this Act in computing the income by way of dividends referred to in section 115BBDA(1)(a).

(3) Meaning of specified assessee [Clause (a) to Explanation under section 115BBDA]:

“Specified assessee” means a person other than,—

-

a domestic company; or

-

a fund or institution or trust or any university or other educational institution or any hospital or other medical institution referred to in sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10; or

-

a trust or institution registered under section 12A or section 12AA.

In other words, all assesses other than a domestic company or a charitable trust approved under section 10(23C) or registered under section 12A or section 12AA shall be liable to pay tax @ 10% on the dividend income received by them in excess of Rs. 10,00,000.

|

7. Tax Treatment of Dividend in the hands of Shareholders : -

Status of the company which

declares dividend |

Taxability in the hands of shareholders |

Dividend distribution tax payable by company which declares dividend |

A : Non-domestic company |

It is taxable in the hands of a shareholder (if it is received in India or if the shareholder is resident and ordinarily resident in India) |

No dividend distribution tax |

B: Domestic company (not being dividend under

section 2(22)(e)j |

General rule - In the hands of shareholder, such dividend is exempt under section 10(34). Exception - From the assessment year 2017-18, dividend income is taxable in the hands of shareholders under section IISBBDA, if a few conditions are satisfied (provisions of

section II5I3BDA are given below) |

The company (which declares dividend) is required to pay dividend distribution tax under section 115-0. It is applicable even if the share- holder is subject to tax under section

II5BBDA |

| C: Domestic company [being loan or advance deemed as dividend under section 2(22)(e)] |

|

|

|

Taxable in the hands of recipient under sec- tion 56 under the head “Income from other sources”

|

No dividend distribution tax under section 115-0

|

- Deemed dividend distri- bution on or after April 1,

2018

|

Not taxable in the hands of recipient by virtue of exemption given by section 10(34) |

The company (which distributes deemed dividend as loan or advance) is liable for dividend distribution tax under section 115-0 at the rate of 30 per cent (+ SC + HEC, effective rate is 34.944 per cent). |

|

|

| |

2. Winnings from Lotteries, Crossword Puzzles, Horse Races and Card Games [Section 56(2)(ib)] |

Under Section 56(2)(ib) of the Indian Income Tax Act, 1961, income from winnings is subject to taxation. This includes income from lotteries, crossword puzzles, horse races, and card games. In this article, we will explore the taxability of such income and the relevant provisions under the Income Tax Act.

Section 56(2)(ib) of the Income Tax Act addresses the taxation of specific kinds of income, which are categorized as "Income from Other Sources." This section pertains to the income earned from the following sources:

1. Winnings from Lotteries:

Any income earned from winnings in lotteries, whether state or non-state lotteries, is considered taxable under Section 56(2)(ib).

Lotteries are a popular form of gambling in India. If you are lucky enough to win a lottery, the winnings will be considered as income and subject to taxation. The income tax rate applicable to lottery winnings is determined based on the individual's income slab. The winnings are added to the individual's total income and taxed accordingly.

2. Winnings from Crossword Puzzles:

Income earned from winning crossword puzzles, game shows, or any similar contests is also subject to taxation under this section.

Crossword puzzles are another form of gambling where individuals can win cash prizes. Similar to lotteries, the income from crossword puzzle winnings is taxable. The winnings are treated as income and added to the individual's total income for the year. The income tax rate applicable will depend on the individual's income slab.

3. Winnings from Horse Races:

Winnings from horse races, including income derived from betting on horse races, fall under the purview of this section.

Horse racing is a popular sport in India, and individuals can place bets on horses. If you are lucky enough to win a bet at a horse race, the winnings are subject to taxation. The income tax rate applicable to horse race winnings is determined based on the individual's income slab. The winnings are added to the individual's total income and taxed accordingly.

4. Winnings from Card Games:

Income from winnings in card games, including games like poker or rummy played in any casino, club, or similar establishments, is taxable as well.

Card games such as poker, rummy, and blackjack are also forms of gambling. If you win a significant amount of money playing card games, the winnings are considered as income and subject to taxation. The income tax rate applicable to card game winnings is determined based on the individual's income slab. The winnings are added to the individual's total income and taxed accordingly.

Key Point of Taxability of Section 56(2)(ib)

Key points regarding the taxability of such income under Section 56(2)(ib) are as follows:

Rate of Tax:

The income earned from the sources mentioned above is taxed at a flat rate of 30% (plus applicable surcharge and cess) as of my last knowledge update. This tax is deducted at source (TDS) by the payer if the winnings exceed a specified threshold.

Threshold for TDS:

The threshold limit for TDS on these winnings may vary depending on the type of game or activity. For example, for horse races, TDS is applicable if winnings exceed Rs. 10,000 in a single race. The specific thresholds should be checked in the latest tax rules.

Reporting:

Taxpayers are required to report such income in their income tax returns and disclose the details of their winnings from lotteries, crossword puzzles, horse races, or card games.

No Deduction Allowed:

Under Section 58(4), no deduction for any expenditure or allowance is allowed against income taxable under Section 56(2)(ib).

Exemptions:

Certain winnings from authorized state lotteries may be exempt from taxation under Section 10(34) and Section 10(34A) of the Income Tax Act. However, specific rules and exemptions may apply and can change with amendments to the tax laws.

Penalties:

Non-compliance with tax regulations, including the provisions of Section 56(2)(ib), can result in penalties and legal consequences.

Tax Deduction at Source (TDS)

It is important to note that tax deduction at source (TDS) is applicable to income from winnings. If the winnings exceed a certain threshold, the payer is required to deduct TDS at the applicable rate before making the payment. The individual receiving the winnings will then receive the net amount after deducting TDS. The TDS amount deducted can be claimed as a tax credit while filing the income tax return.

Although, winnings from lotteries, etc. is part of total income of the assessee, such income is taxable at a special rate of Income-tax, which at present, is 30% + surcharge, if applicable + health and education cess 4%.

Deduction of any expenses, allowance or loss not allowed from such winnings: According to section 58(4), no deduction in respect of any expenditure or allowance, in connection with such income, shall be allowed under any provision of the Income-tax Act. However, expenses relating to the activity of owning and maintaining race horses are allowable.

In other words, the entire income of winnings, without any expenditure or allowance, will be taxable. In fact, deduction under sections 80C to 80U discussed later in the Chapter on Deductions from Gross Total Income will also not be available from such income although such income is a part of the total income.

As lottery income is taxed at flat rate, the basic exemption of income (say Rs. 2,50,000) is not available to the assessee.

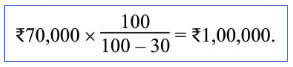

As in the case of some other incomes, there is also a provision for tax to be deducted at source from income from winning of lotteries, horse races and crossword puzzles. The rate of TDS in the case of such incomes is 30% if the income exceeds Rs. 10,000. Such tax deducted at source is income and the amount received is net income after deduction of tax at source. In this case, such net income will have to be grossed up as under:

If a person wins a lottery of Rs. 1,00,000, tax must have been deducted @ 30% and net amount received by the assessee would be Rs. 70,000 (1,00,000 – 30,000).

Grossing up would be done as:

Conclusion

Income from winnings from lotteries, crossword puzzles, horse races, and card games is subject to taxation under Section 56(2)(ib) of the Indian Income Tax Act, 1961. The income tax rate applicable will depend on the individual's income slab. It is important to keep track of such winnings and ensure compliance with the income tax provisions. Additionally, TDS may be applicable if the winnings exceed a certain threshold, and the net amount received after deducting TDS can be claimed as a tax credit. |

|

3. Interest on Securities under the head 'Income from Other Sources' [Section 56(2)(id)] |

1. Meaning of Interest on Securities

Income, by way of interest on securities, is chargeable under the head "income from other sources", if such income is not chargeable to income-tax under the head, "Profits and Gains of Business or Profession".

According to Section 2(28B) "Interest on securities" means:

-

Interest on any security of the Central Government or a State Government;

-

Interest on debentures or other securities for money issued by, or on behalf of a local authority or a company or a corporation established by Central, State or Provincial Act.

Thus securities may be divided into following categories:

-

Securities issued by Central/State Governments;

-

Debentures/bonds issued by a local authority;

-

Debenture/bonds issued by companies;

-

Debenture/bonds issued by a corporation established by a Central, State or Provincial Act i.e. autonomous and statutory corporations.

|

2. Chargiability of Interest on Securities :

-

Income by way of interest on securities is taxable on “receipt” basis, if the assessee maintains books of account on “cash basis”.

-

It is taxable on “due” basis when books of account are maintained on mercantile system.

-

Interest is taxable on “receipt” basis, if such interest had not been charged to tax on due basis for any earlier previous year.

3. Accrual of Interest on Securities :

Interest on securities does not accrue everyday or according to the period of holding of investment. For instance, if one holds 7% securities from January 1, 2019 to February 28, 2019, it cannot be said that interest of two months has accrued to the security holder. Generally, interest becomes due on due dates specified on securities. For instance..., if specified due dates of interest of particular securities are March 1 and September 1 every year, interest of six months falls due on each such date and holder of securities on these dates will be entitled to interest of six months on each such date.

For instance :

If X purchases 7% Rs. 20,000 Securities (specified due dates: March 1 and September 1) on February 25, 2019 and sells the same on March 2, 2019, he will become entitled for interest of 6 months (i.e., Rs. 20,000 × ½ × 7 ÷ 100 = Rs. 700), irrespective of the fact that he holds Securities just for 6 days. As, in this case, interest of 6 months has become due to X on March 1, 2019, he will be liable to pay tax on the entire interest of Rs. 700 in the previous year 2018-19 if he maintains books of account on “mercantile system”. If, however, X maintains books of account on “cash” system, then Rs. 700 is taxable in the previous year in which it is received.

4. Grossing up of Interest on Securities :

Gross interest [i.e., Net Interest + TDS (Tax Deducted at Source] is Taxable.

Net interest is grossed up in the hands of recipient if tax is deducted at source by the payer.

Net interest (if tax is deducted at source) in the hands of the recipient should be grossed up by multiplying it by the following fraction :

Net Interest x 100 ÷ [100 - Rate of TDS (tax deduction at source)]

Grossing up is required in the case of the following securities:—

-

8% Saving (Taxable) Bonds if the amount of interest payable exceeds Rs.10,000 (these Bonds have now been withdrawn. New 7.75% Government of India Savings (Taxable) Bonds, 2018 have been issued);

-

securities issued by a statutory corporation or a local authority or by any company.

|

5. Deductions for Expenses from Interest on Securities [Section 57(i) and (iii)]:

As discussed in the case of dividends, the following deductions will also be allowed from the gross interest on securities:

-

Collection charges [Section 57(i)]:

Any reasonable sum paid by way of commission or remuneration to a banker, or any other person for the purpose of realising the interest.

-

Interest on loan [Section 57(iii)]:

Interest on money borrowed for investment in securities can be claimed as a deduction.

-

Any other expenditure [Section 57(iii)]:

Any other expenditure, not being a expenditure of a capital nature, expended wholly and exclusively for the purpose of making or earning such income can be claimed as a deduction.

|

6. Avaoidance of Tax in respect of Interest on Securities (Section 94)

Interest on securities does not accrue from day to day but on certain fixed dates. If, on the eve of due date of payment of interest, a person transfers securities to another person and reacquires the same or similar securities after interest has been received by the transferee, the transferor would be able to evade tax in respect of such interest. To prevent this malpractice, section 94 provides certain checks under sub-sections (1) and (2).

(A) Bond Washing Transactions [Section 94(1)]-

A bond washing transaction is narrated as a transaction which consists of selling securities (to a friend or relative) some time before the due date and acquiring back the same (or similar) securities after the due date of interest is over. This practice is generally adopted by high-income class assessees to evade the tax while transferring securities to low-income class assessees on the eve of due date of payment of interest. If this practice is not checked, interest is includible in the total income of the transferee, as interest is chargeable in the hands of the person who is legal owner of securities on the due date of payment of interest.

To prevent the avoidance of tax in this manner, section 94(1) provides that where a security owner transfers the securities on the eve of due date of interest and reacquires them, the interest received by the transferee will be deemed as income of the transferor and, accordingly, it will be included in the total income of the transferor and not of the transferee.

(B) Sales Cum-Interest on Securities [Section 94(2)] -

Another method of avoiding tax is sale of securities cum-interest. Section 94(2) provides that if an assessee, having beneficial interest in securities during the previous year, sells them in such a way that either no income is received or income received is less than the sum he would have received if interest had accrued from day to day, then income from such securities for such year would be deemed as income of such person.

EXCEPTIONS -

Deeming provisions of section 94(1)/(2), discussed above, are not applicable if the security owner proves to the satisfaction of the Assessing Officer that —

-

There has been no avoidance of income-tax; or

-

The avoidance of income-tax was exceptional and not systematic and there was not any avoidance of incometax under section 94(1)/(2) in his case, during three years preceding the previous year.

|

|

| |

4. Income from Letting Out of Machinery , Plant or Furniture [Section 56(2)(ii)] |

Income from machinery, plant or furniture, belonging to the assessee and let on hire, is chargeable as income from other sources, if the income is not chargeable to income-tax under the head "Profits and Gains of Business or Profession".

( In case any such assets are hired out as a part of the business activity carried on by the assessee or as commercial assets belonging to the assessee, the income derived therefrom is assessable as business income under section 28 and not as Income from other sources under section 56 )

5. Income from Composite Letting of Machinery, Plant or Furniture and Buildings [Section 56(2)(iii)]:

If an assessee lets on hire machinery, plant or furniture and also building and letting of building is inseparable from letting of machinery, plant or furniture, income from such letting is taxable as income from other sources, if the same is not chargeable to tax under the head “Profits and gains of business or profession”.

On the basis of the judicial pronouncements, the following broad conclusions can be drawn:

-

If there is letting of machinery, plant and furniture and also letting of the building and the two lettings form part and parcel of the same transaction or the two lettings are inseparable (in the sense that letting of one is not acceptable to the other party without letting of the other; for instance, letting of cinema house along with letting of furniture) then such income is taxable under section 56(2)(iii) under the head “Income from other sources” (if it is not taxable as business income). This rule is applicable even if sum receivable for the two lettings is fixed separately.

-

If a building is let out but other assets like machinery, plant or furniture are not given on rent. However, certain amenities like lift services, air-conditioning, fire fighting facilities, etc., are provided, then section 56(2)(iii) is not applicable. The essential requirement of section 56(2)(iii) is that there should be letting of plant, machinery or furniture and also letting of building.

For instance, if the owner of a building only undertakes to instal and operate an air-conditioning plant and to instal, and maintain a lift in the building for the benefit of all the tenants at specified charges (maybe on “no profit no loss basis” or some other basis), there is no letting of air-conditioning plant and lifts to the tenants. Consequently, in such case incomes from letting of building is taxable under section 22 under the head “Income from house property” and amount collected for providing different amenities shall be taxable under section 56(1).

The aforesaid rule is applicable even if the assessee receives composite rent from his tenant towards building as well as services/amenities. The portion of rent attributable to the building should only be assessed as “Income from house property” and balance portion attributable to amenities must be assessed as “Income from other sources”.

1. Deductions permissible from Letting out of Machinery, Plant or Furniture and Buildings [Section 57(ii) and (iii)]:

The following deductions are allowable:

-

Current repairs, to the premises held otherwise than as tenant.

-

Insurance premium against risk of damage or destruction of the premises.

-

Repairs and insurance of machinery, plant or furniture.

-

Depreciation based upon block of assets, in the same manner as allowed under section 32 in the case of Income from Business and Profession subject to the provisions of section 38 i.e. if it is partly let and partly used for own purpose, deduction of expenses (including depreciation) shall be allowed to the extent it is let out.

-

Any other expenditure: Any other expenditure, not being a expenditure of a capital nature, laid out or expended wholly and exclusively for the purpose of making or earning such income can be claimed as a deduction.

|

|

6. Share Premium in excess of the Fair Market Value to be treated as Income [Section 56(2)(viib)] |

Section 56(2)(viib) is applicable as follows –

-

Recipient is a company (not being a company in which the public are substantially interested).

-

It receives consideration for issue of shares (preference shares or equity shares) from a resident person.

-

The consideration received for issue of shares exceeds the face value of such shares. In other words, shares are issued at a premium.

If the above conditions are satisfied, the aggregate consideration received for such shares as exceeds the fair market value of the shares, shall be chargeable to income-tax in the hands of recipient-company under section 56(2)(viib) under the head “Income from other sources”.

The above provisions are not applicable in the following two cases –

-

where the consideration for issue of shares is received by a venture capital undertaking from a venture capital company or a venture capital fund; or

-

where the consideration for issue of shares is received by a company from a class or classes of person as notified† by the Central Government.

The fair market value of the shares shall be the higher of the value—

-

as may be determined in accordance with the method given in rules 11U and 11UA ; or

-

as may be substantiated by the company to the satisfaction of the Assessing Officer, based on the value of its assets, including intangible assets, being goodwill, know-how, patents, copyrights, trademarks, licences, franchises or any other business or commercial rights of similar nature.

|

|

7. Interest on Compensation or Enhanced Compensation [Section 56(2)(viii)]

As per section 145A(b), any interest received by an assessee on compensation or enhanced compensation, as the case may be, shall be deemed to be the income of the year in which it is received.

Further, as per section 56(2)(viii), income by way of interest received on compensation or on enhanced compensation referred to in section 145A(b) above shall be taxable under the head income from other sources in the previous year in which such interest is received.

Deduction from such interest [Section 57(iv)]:

In the case of above interest which is taxable under the head income from other sources, a deduction of a sum equal to 50% of such income shall be allowed to the assessee and no deduction shall be allowed under any other clause of section 57.

Example :

Mr. X whose property was compulsorily acquired in 2013 received enhanced compensation of Rs. 9,00,000 on 15.11.2017 which includes Rs.2,40,000 as interest on such enhanced compensation. Discuss the taxability of such compensation.

Solution:

Enhanced compensation of Rs. 9,00,000 – Rs. 2,40,000 = Rs. 6,60,000 shall be taxable under the head capital gain. Whereas interest on enhanced compensation shall be taxable under the head income from other sources as under:

| Particulars |

Amount (Rs.) |

| Interest on Enhanced Compensation Received |

2,40,000 |

| Less : Deduction @ 50% |

1,20,000 |

| Balance Taxable |

1,20,000 |

|

| |

8. Forfeiture of Advance Received for Transfer of a Capital Asset to be Taxed under the head "Income from Other Sources" [Section 56(2)(ix)]

According to section 56(2)(ix), any sum of money, received as an advance or otherwise in the course of negotiations for transfer of a capital asset shall now be taxable under the head income from other sources if:

- Such sum is Forfeited; and

- The negotiations do not result in transfer of such capital asset.

|

9. Income of any Person to include not only Gift of Money from any person(s) but also the Gift of Property (whether Movable or Immovable) or Property acquired for inadequate consideration [Section 56(2)(x), w.e.f. A.Y. 2018-19]

(1) Where any Person Receives, in any previous year, from any Person or Persons on or after 1.4.2017 :

The following income, it shall be chargeable to income tax under the head "income from other sources" as per section 56(2)(x):

| Particulars of Income |

Amount Taxable under the head 'Income from Other Sources' |

(A) Any sum of money,—

— without consideration, the aggregate value of which exceeds Rs. 50,000 |

The whole of the aggregate value of such sum |

(B) Any immovable property,—

(i) without consideration, the stamp duty value of which exceeds Rs. 50,000; |

The Stamp Duty Value of such property |

(ii) for a consideration which is less than the stamp duty value of the property by an amount exceeding Rs. 50,000. |

the stamp duty value of such property as exceeds the consideration received |

(C) Any property, other than immovable property,—

(i) without consideration, the aggregate fair market value of which exceeds Rs. 50,000; |

The whole of the aggregate fair market value of such property

|

(ii) for a consideration which is less than the aggregate fair market value of the property by an amount exceeding Rs. 50,000: |

The aggregate fair market value of such property as exceeds such consideration |

-

"Fair market value" of a property, other than an immovable property, means the value determined in accordance with the method as may be prescribed.

-

"Property" means the following capital asset of the assessee, namely:—

- immovable property being land or building or both;

- shares and securities;

- jewellery;

- archaeological collections;

- drawings;

- paintings;

- sculptures;

- any work of art; or

- bullion;

Amendment made by the Finance Bill, 2022 :

Explanation to Section 56(2)(x) Amended [w.e.f. AY 2023-24]

In order to provide for taxing the gifting of virtual digital assets, the Finance Bill, 2022 has amended Explanation to section 56(2)(x) of the Act to inter-alia, provide that for the purpose of the said clause, the expression “property” shall have the meaning assigned to it in Explanation to section 56(2)(vii) and shall include virtual digital asset. |

(2) Section 56(2)(x), Not to Apply in certain cases

Section 56(2)(x), shall not apply to any sum of money or any property received—

-

from any relative; or

-

on the occasion of the marriage of the individual; or

-

under a will or by way of inheritance; or

-

in contemplation of death of the payer or donor, as the case may be; or

-

from any local authority as defined in the Explanation to section 10(20); or

-

from any fund or foundation or university or other educational institution or hospital or other medical institution or any trust or institution referred to in section 10(23C); or

-

from or by any trust or institution registered under section 12A or section 12AA; or

-

by any fund or trust or institution or any university or other educational institution or any hospital or other medical institution referred to in section 10(23C)(iv) or (v) or (vi) or (via); or

-

by way of transaction not regarded as transfer under section 47(i) or (vi) or (via) or (viaa) or (vib) or (vic) or (vica) or (vicb) or (vid) or (vii); or

|

|

| |

") |

|

| |

|

|

@ Rs.700")

@ Rs.700")

@ Rs.600")

@ Rs.550")